#home Insurance

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

US Tumblr user growth rate is estimated to slow down to 4.1%.

Text

Excerpt from this story from the New York Times:

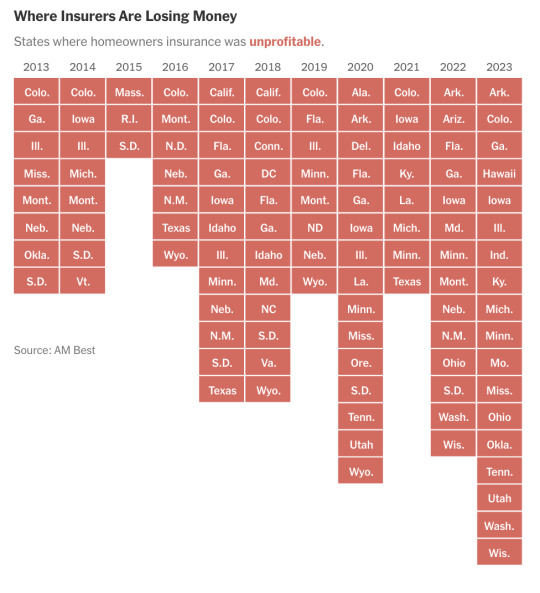

At first glance, Dave Langston’s predicament seems similar to headaches facing homeowners in coastal states vulnerable to catastrophic hurricanes: As disasters have become more frequent and severe, his insurance company has been losing money. Then, it canceled his coverage and left the state.

But Mr. Langston lives in Iowa.

Relatively consistent weather once made Iowa a good bet for insurance companies. But now, as a warming planet makes events like hail and wind storms worse, insurers are fleeing.

Mr. Langston spent months trying to find another company to insure the townhouses, on a quiet cul-de-sac at the edge of Cedar Rapids, that belong to members of his homeowners association. Without coverage, “if we were to have damage that hit all 17 units, we’re looking at bankruptcy for all of us,” he said.

The insurance turmoil caused by climate change — which had been concentrated in Florida, California and Louisiana — is fast becoming a contagion, spreading to states like Iowa, Arkansas, Ohio, Utah and Washington. Even in the Northeast, where homeowners insurance was still generally profitable last year, the trends are worsening.

In 2023, insurers lost money on homeowners coverage in 18 states, more than a third of the country, according to a New York Times analysis of newly available financial data. That’s up from 12 states five years ago, and eight states in 2013. The result is that insurance companies are raising premiums by as much as 50 percent or more, cutting back on coverage or leaving entire states altogether. Nationally, over the last decade, insurers paid out more in claims than they received in premiums, according to the ratings firm Moody’s, and those losses are increasing.

The growing tumult is affecting people whose homes have never been damaged and who have dutifully paid their premiums, year after year. Cancellation notices have left them scrambling to find coverage to protect what is often their single biggest investment. As a last resort, many are ending up in high-risk insurance pools created by states that are backed by the public and offer less coverage than standard policies. By and large, state regulators lack strategies to restore stability to the market.

Insurers are still turning a profit from other lines of business, like commercial and life insurance policies. But many are dropping homeowners coverage because of losses.

Tracking the shifting insurance market is complicated by the fact it is not regulated by the federal government; attempts by the Treasury Department to simply gather data have been rebuffed by some state regulators.

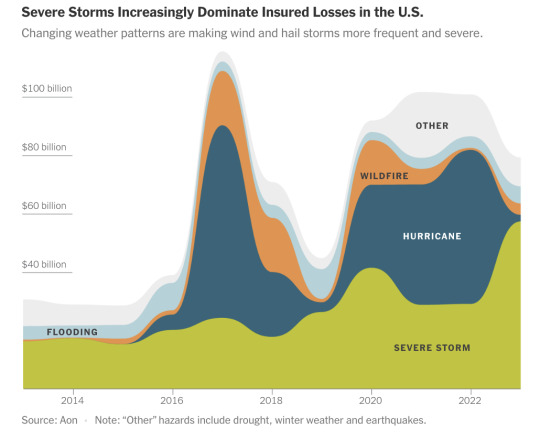

The turmoil in insurance markets is a flashing red light for an American economy that is built on real property. Without insurance, banks won’t issue a mortgage; without a mortgage, most people can’t buy a home. With fewer buyers, real estate values are likely to decline, along with property tax revenues, leaving communities with less money for schools, police and other basic services.

And without sufficient insurance, people struggle to rebuild after disasters. Last year, storms, wildfires and other disasters pushed 2.5 million American adults out of their homes, according to census data, including at least 830,000 people who were displaced for six months or longer.

121 notes

·

View notes

Text

#tiktok#California#tw fire#home insurance#palisades fire#capitalism kills#capitalism is evil#capitalism is a scam#capitalism is a disease#capitalism is hell#climate change#climate crisis

18 notes

·

View notes

Text

Cindy Picos was dropped by her home insurer last month. The reason: aerial photos of her roof, which her insurer refused to let her see.

“I thought they had the wrong house,” said Picos, who lives in northern California. “Our roof is in fine shape.”

Her insurer said its images showed her roof had “lived its life expectancy.” Picos paid for an independent inspection that found the roof had another 10 years of life. Her insurer declined to reconsider its decision.

Across the U.S., insurance companies are using aerial images of homes as a tool to ditch properties seen as higher risk.

Nearly every building in the country is being photographed, often without the owner’s knowledge. Companies are deploying drones, manned airplanes and high-altitude balloons to take images of properties. No place is shielded: The industry-funded Geospatial Insurance Consortium has an airplane imagery program it says covers 99% of the U.S. population.

The array of photos is being sorted by computer models to spy out underwriting no-nos, such as damaged roof shingles, yard debris, overhanging tree branches and undeclared swimming pools or trampolines. The red-flagged images are providing insurers with ammunition for nonrenewal notices nationwide.

“We’ve seen a dramatic increase across the country in reports from consumers who’ve been dropped by their insurers on the basis of an aerial image,” said Amy Bach, executive director of consumer group United Policyholders.

The increasingly sophisticated use of flyby photos comes as home insurers nationwide scramble to “derisk” their property portfolios, dropping less-than-perfect homes in an effort to recover from big underwriting losses.

(continue reading)

56 notes

·

View notes

Text

2 notes

·

View notes

Text

Why did you buy a house? Metropolitan Life Insurance Company ad - 1958.

#vintage illustration#vintage advertising#insurance#home insurance#insurance companies#met life#metlife#metlife insurance#metropolitan life insurance company#metropolitan life insurance#metropolitan life

3 notes

·

View notes

Text

Find the Cheapest Travel Insurance for Schengen Visa:

Introduction to Schengen Travel Insurance

Once in Europe traveling is full of excitement. But, it’s significant to be well-protected. Schengen travel insurance is not something that is suggested as an option, it is rather a mandatory requirement which is made compulsory for all Schengen visa applicants. Besides healthcare, it also protects passengers from such types of expenses as trip cancellations and other unforeseen contingencies. Let’s explore the Cheapest Travel Insurance for Schengen Visa in this article.

Understanding Cheapest Travel Insurance for Schengen Visa Requirements

In particular, the insurance policy that is compulsory when applying for the Schengen visa is vital when arranging your European trip. The policy should insure at least €30,000 for the medical expenses and the repatriation returning the insurance sum to the insurance company. It must provide you with pass-free access to all Schengen countries for the entire period of your stay.

The Importance of Travel Insurance for Schengen Visa Applicants

Securing travel insurance is not merely a tick off of the “to have” list, but a support that is there for the times when you need it the most. In this way, the provider is prevented from the situations of not going anywhere like emergency happenings, robbery, or the hurdles of the trip.

Selecting the Right and Cheapest Travel Insurance for Schengen Visa Plan

Deciding the best insurance plan may be a challenge but it’s important to forget about possible uncertainties during a trip. The following is an explanation of how to choose an insurance package that covers the essentials with a budget in mind and how to find Cheapest Travel Insurance for Schengen Visa.

2 notes

·

View notes

Text

Phone: (858) 569-1009

Address: 10769 Woodside Ave Ste 103, Santee, CA 92071, United States

Email: [email protected]

LOCAL INSURANCE AGENCY OFFERING ALL LINES OF INSURANCE. AUTO INSURANCE, HOME INSURANCE, RENTERS INSURANCE, MOBILE HOME INSURANCE, MANUFACTURED HOME INSURANCE, LIFE INSURANCE, BUSINESS INSURANCE, WORKERS COMP

2 notes

·

View notes

Text

How to Choose the Right Home Insurance in the UAE?

Home insurance is a type of property insurance that covers losses and damage that occur to an individual’s house or insured belongings. The coverage can cover costs due to natural calamities such as floods and earthquakes. Plus, it covers fire-related damages to the property.

Although the UAE is one of the safest places, the absence of home insurance can put a huge financial burden on people for rebuilding. In this blog, find out how to choose the right home insurance in the UAE.

Understand Insurance Needs

The first step is to understand personal insurance needs. The location of the residence is one of the major factors one should consider while opting for a home insurance policy. In addition, decide if you want insurance coverage only for the property or the belongings in the house or both. Other factors such as age, income, health, employment, settlement plan, family and more can be considered too.

Do Research

Do your own research about the different insurance companies. Find out the following about the insurance providers:

Company Reputation

Financial Stability

Customer Service

Claim Settlement Time

Search online for reviews, customer feedback and ratings. Seek help from friends and families. Else, get expert advice from insurance experts in the UAE. Also, it is important that the insurance provider has a licence as per the laws in the UAE.

Compare Different Home Insurance Policies

Once you narrow down the list of insurance companies, start comparing different home insurance policies offered. Read carefully each and every detail to have a complete understanding of the insurance coverage promised. Plus, read the terms and conditions thoroughly. Compare the procedures to claim insurance and the time required to achieve a settlement.

Consider the Features

Find out if there are additional benefits or add-ons offered by the insurance company in addition to the standard coverage. It is necessary to cover specific needs besides basic coverage. However, one of the main factors to consider is the cost. Take time and assess if the add-ons are worth the additional money.

Budget

The cost of a home insurance policy is one of the key factors that distinguish one insurer from another. Compare the following things to find the best insurance policy that provides the best value:

Premium

Deductible Amounts

Exclusions

Discuss if there are discounts or promotions that can significantly lower the cost and boost savings on insurance.

Review

Periodical review of the home insurance is essential to meet the changing needs and the coverage required. The best thing is to review annually if the insurance coverage is enough for the future.

Claim Rejection

Make sure to submit all the necessary documents and provide all the necessary details to avoid claim rejection when one needs it the most. As world events become more unpredictable, choosing a home insurance policy can keep everyone protected. Crossroads Insurance Brokers is a leading insurance broker in the UAE offering cutting-edge insurance solutions. Contact us for more details.

#property insurance#insurance broker in the UAE#home insurance#property insurance in UAE#personal insurance

2 notes

·

View notes

Text

NLP Practitioner Program in India | Benefits of NLP Training & Coaching

Enrolling in an NLP Practitioner Program in India is a life-changing decision for those who want to enhance their communication skills, overcome self-limiting beliefs, and develop a success-oriented mindset. NLP (Neuro-Linguistic Programming) is a powerful tool that helps individuals reshape their thought patterns, improve emotional intelligence, and achieve their personal and professional goals. With the right training, anyone can master the techniques of NLP and apply them effectively in different areas of life.

The NLP Practitioner Program in India is designed to provide in-depth knowledge and hands-on experience with proven techniques like anchoring, reframing, and rapport-building. These strategies help individuals gain confidence, improve problem-solving skills, and communicate more effectively in personal and professional settings. Whether you are a coach, entrepreneur, corporate leader, or therapist, NLP training equips you with the skills to influence and inspire those around you. By learning NLP, you develop the ability to shift focus from obstacles to opportunities, making it an essential tool for self-improvement. These techniques are widely used by business leaders, life coaches, and psychologists to enhance productivity, build stronger relationships, and develop a growth mindset. The skills you gain will help you navigate challenges, build resilience, and achieve extraordinary success.

Start your transformation today! Enroll in an NLP Practitioner Program in India and take the first step toward personal and professional excellence.

#want to become lic agent in delhi#insuranceagent#agent#how to apply for lic agent in delhi#financial planning#career#how to become lic agent in delhi#how to join lic as an agent#insurance#join us#insurance agent#insurance advisor#healthcare#health insurance#medicine#home insurance#insurance policy#personal loans#loans#business loans#financial

0 notes

Text

Home Insurance Made Easy: Tips to Protecting Your Home

What is home insurance and why do I need it?

Home insurance provides financial protection against damage or loss to your home and personal belongings due to events like fire, theft, or natural disasters. It also offers liability coverage if someone is injured on your property. While not legally required, most mortgage lenders mandate it to protect their investment.

How do I choose the right home insurance policy?

Selecting the appropriate policy involves assessing your home's value, the cost to rebuild, and the value of your personal belongings. Consider additional coverage for high-value items and natural disasters common in your area. Comparing quotes from multiple insurers can help you find a policy that balances coverage and cost effectively.

What factors affect my home insurance premium?

Several factors influence your premium, including the age and condition of your home, its location, the materials used in construction, your credit score, and the amount of coverage you select. Implementing safety measures like installing smoke detectors, security systems, and fire-resistant materials can potentially lower your premium.

Does home insurance cover natural disasters?

Standard home insurance policies typically cover damage from events like fire, windstorms, and hail. However, coverage for natural disasters such as floods, earthquakes, or hurricanes may require additional endorsements or separate policies. It's essential to review your policy and consider adding coverage for specific risks prevalent in your area.

How can I lower my home insurance costs?

To reduce your premium, consider increasing your deductible, bundling home and auto insurance policies, maintaining a claims-free history, and implementing home security measures. Regularly reviewing and updating your policy to reflect changes in your home's value and condition can also help ensure adequate coverage at a competitive rate.

#home insurance#house insurance#home insurance quotes#homeowners insurance#home insurance companies.

1 note

·

View note

Text

Get affordable and reliable auto insurance in Edmonton with Corey Scales, your trusted Desjardins Insurance Agent. Offering comprehensive coverage for auto, home, life, and business insurance, along with specialized options like snowmobile, ATV, motorcycle, and boat insurance. We provide personalized service in English, Punjabi, Hindi, Mandarin, and Cantonese. Call 780-757-1176 for your free auto insurance quote today!

#Insurance#Personal Finance#Auto Insurance In Edmonton#Auto Insurance#home insurance#business insurance#life insurance#Dental insurance

1 note

·

View note

Text

[10 Jan 2025, by Kate Aronoff]

Popular narrative suggests insurance companies have to raise rates due to fire risk. In reality, the companies are doing pretty well.

The day that Hurricane Andrew touched down in Florida in 1992, J.W. Greenberg—executive vice president of the finance and insurance giant American International Group, or AIG—sent a memo around to company staff. “This is an opportunity,” he wrote, “to get price increases now. We must be the first, and it begins by establishing the psychology with our own people. Please get it moving today.”

To date, no such memos have surfaced about the fires now engulfing Los Angeles County, where at least five people have died and tens of thousands remain under evacuation orders from Santa Clarita to Santa Monica. Preliminary estimates from JPMorgan predict that damages could soar to $50 billion. Thanks to recent regulatory changes in California’s insurance market, though—including some pushed through as recently as late December—insurers there could find it easier to extract the kinds of price increases Greenberg was talking about.

Standard mainstream media accounts of California’s insurance market warn of a virtually existential “crisis” facing insurers that operate in the state, who are grappling with “profound financial strain” amid mounting losses from climate-fueled wildfires. Citing these pressures, AllState and State Farm both announced in 2023 that they would stop issuing new homeowners insurance policies, and move to shed existing policies. State Farm announced last March that it would not renew 72,000 existing California property insurance policies, including in some of the places worst hit by the fires still blazing in L.A. An investigation by the San Francisco Chronicle found that the company planned to scrap more than 69 percent of its policies in the well-heeled Pacific Palisades neighborhood, much of which now stands in ruins. Overall, California last year had the fourth-highest rate of nonrenewal in the country after Florida, Louisiana, and North Carolina.

Insurers in California did indeed face considerable losses due to wildfires in 2017 and 2018, when damages from the Camp, Tubbs, and Woolsey fires totaled $23 billion. California, however, has in recent years been among the country’s most lucrative states for companies that sell homeowners multi-peril insurance, a product that covers wildfire damages. Data collected by S&P Global Intelligence on statewide loss ratios—essentially, the percentage of premium income that insurers pay out to cover insured losses—shows that insurers offering homeowners multi-peril insurance in California had a loss ratio of 53.7 percent in 2022 and 61.3 percent in 2023. That’s compared to nationwide loss ratios of around 70 percent in each year. In other words, home insurers in California had a significantly larger share of their income from premiums left over after paying out policyholders. State Farm actually outperformed statewide average loss ratios in both years.

0 notes

Text

0 notes